The Reality of Floods and Flood Insurance

The risks associated with flooding are real, and it affects more people than many realize. Flooding can happen to anyone at anytime anywhere it rains. These realities will clear up some misconceptions about flooding and flood insurance and help you better understand your flood risk and policy options.

Myth: Only homeowners can purchase flood insurance.

Reality: Most homeowners, condo unit owners, renters and businesses in National Flood Insurance Program (NFIP) participating communities can purchase flood insurance. To find out if your community participates, go to http://www.floodsmart.gov or contact a community official or insurance agent.

Myth: If you are not in a high-risk area, you don't need flood insurance.

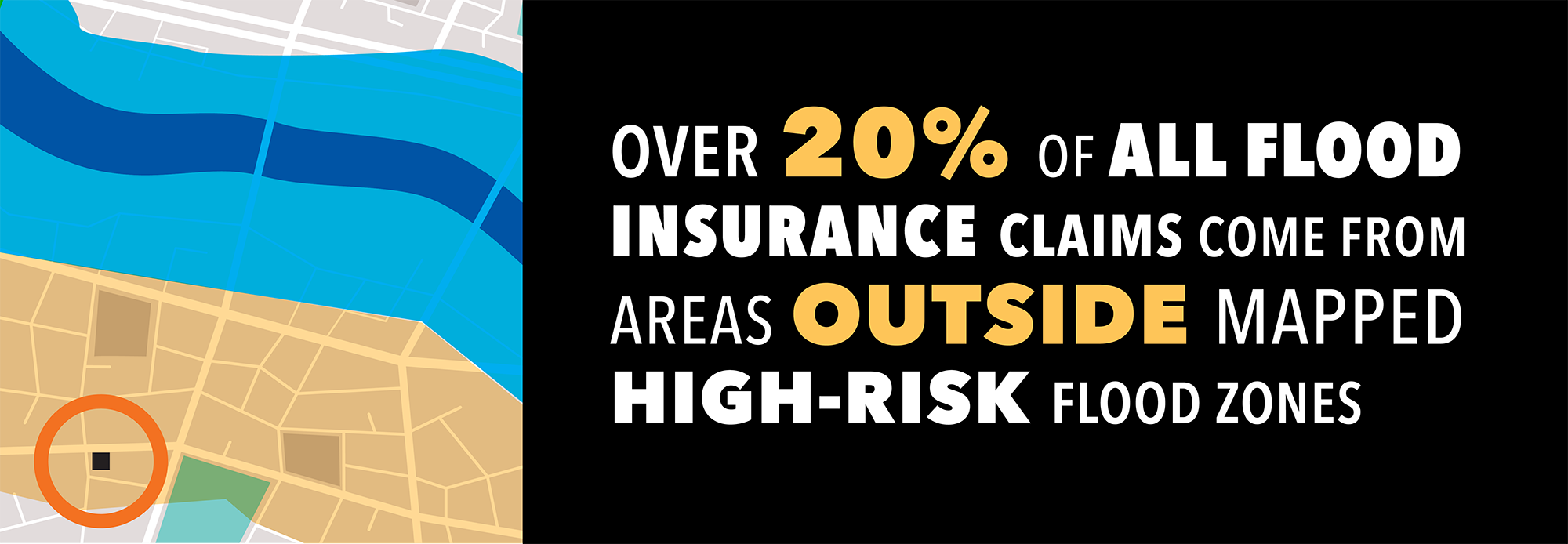

Reality: While mortgage companies typically do not require flood insurance for homes outside high-risk areas, more than 20 percent of the NFIP's claims come from outside mapped flood zones.

Over 20% of all flood insurance claims come from areas outside mapped high-risk flood zones.

Myth: My homeowners insurance covers me against floods.

Reality: Most homeowners and business insurance policies do not cover flooding.

Myth: All flood insurance is the same price.

Reality: The price for flood insurance varies by provider and proximity to flood zones.

Myth: You can't buy flood insurance if your property flooded before.

Reality: If your community participates in the NFIP, you are still eligible to purchase a flood insurance policy, regardless of flood history.

Myth: You can buy flood insurance immediately before a flood and be covered.

Reality: While you can purchase flood insurance from the National Flood Insurance Program at any time, there is usually a 30-day waiting period before the policy takes effect. Your new policy will only cover losses that occurred after the policy takes effect. For more information, visit https://www.floodsmart.gov/faqs.

Myth: I live in a 100-year floodplain, so there is very little chance of flooding.

Reality: During a 30-year mortgage, you are 27 times more likely to experience a flood than have a fire.

During a 30-year mortgage you are 27 times more likely to experience a flood than a fire.

Myth: My home will be fine once it dries out.

Reality: Flooding can cause damage to the foundation of a house and penetrate the walls and subfloors, causing mold and other problems.

Myth: The Federal Government offers a variety of types of disaster recovery assistance. There are different types of assistance that benefit individuals in addition to individual assistance.

Reality: Federal assistance varies, but may be available to state, local, tribal and territories, certain types of private nonprofit organizations and faith-based organizations, and to individuals and households. The SBA, HUD, USDA, and U.S. Department of Commerce may also have applicable assistance programs. Specifically, through FEMA’s Individuals and Households Program (IHP) programs, FEMA provides direct assistance to individuals and households, as well as state, local, tribal and territories governments to support individual survivors. For more information, visit https://www.fema.gov/individual-disaster-assistance.

Myth: Everyone is eligible for FEMA assistance.

Reality: After a Presidential declaration, disaster assistance may available for eligible disaster survivors in the form of financial housing assistance such as rental assistance, lodging expense reimbursement, and home repair or replacement assistance; and Direct Housing Assistance, in the form of manufactured housing units, multi-family lease and repair, and permanent or semi-permanent housing construction. These funds and programs are dispersed through FEMA’s Individuals and Households Program (IHP) and financial assistance provided should be used to bring damaged homes back to safe and sanitary living conditions. However, while federal disaster assistance grants are available, assistance is generally more typically a low-interest disaster loan from the Small Business Administration. For more information, visit https://www.sba.gov/funding-programs/disaster-assistance.

Myth: Signing an assignment of benefit (AOB) agreement, which assigns insurance claim rights to a third party, is a fast way to recover from a storm or flood loss.

Reality: An assignment of benefit agreement can be a great tool. But it is a legal document. Contact your insurance company before you sign away your benefits.

An assignment of benefits can be a great tool, but it is a legally binding contract.

Myth: An AOB is my only option when recovering from a loss.

Reality: Signing an AOB is not your only choice. Contact your insurance company to understand your options.

Myth: If I want to cancel an AOB agreement, I can easily back out.

Reality: A properly executed AOB is a binding contract. You may have to get legal assistance to regain control over the insurance benefits.